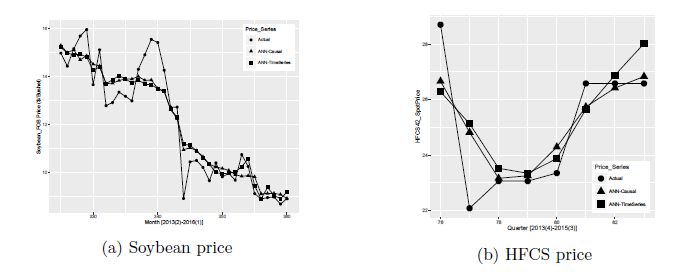

Abstract

This paper uses artificial neural networks to evaluate the performance of soybean and high fructose corn syrup (HFCS) price forecasting using both causal and time series techniques. Mean absolute deviation, and mean square error (both in–sample and out–of–sample) are used to evaluate the predictive accuracy of causal and time series neural networks. Based on the out–of–sample forecast performance, causal neural networks performed better in predicting both soybean and HFCS prices. To check the robustness of the results, a turning point test and sensitivity analysis are conducted. A turning point test is performed to evaluate the technique that captures the most turning points. Turning point test results indicate that the time series forecasting approach captures the most turning points for both soybean and HFCS prices. Finally, a sensitivity analysis is performed to analyze the relative importance of explanatory variables on soybean and HFCS prices. Results of this article help to guide forecasting approach selection based on research objectives.